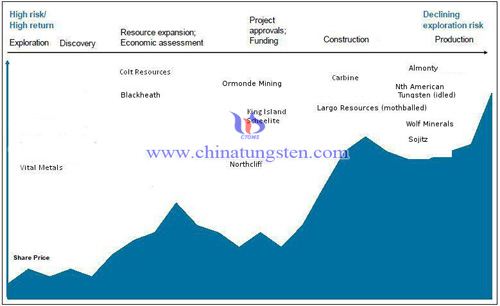

The Tungsten Lifecycle Chart

- Details

- Category: Tungsten's News

- Published on Friday, 13 November 2015 14:14

Our all-purpose Lifecycle chart serves particularly well, in the case of Tungsten, to show the state of progress of the various players vis-à-vis each other on the exploration-production continuum (not that some players, irrespective of which metal, imagine themselves production-bound).

This chart raises the interesting question of how to deal with juniors. During the years of the Supercycle any junior in a given metal could be seen as a potential player. As it wended its way through the Resource/PEA/PFS/BFS continuum there was always an assumption that financing would be forthcoming by hook or by crook for a worthy project. That is now not the case. So do we position a no-hope junior on the Lifecycle Chart at all or just cast them into the outer darkness?

The second issue relates to “naming names” because it is not particularly a company that it somewhere on the timeline but rather individual projects. A good example is Almonty, which has a producing mine in Spain, a near producing mine in Australia and a more distant prospect in South Korea. The stricken North American Tungsten has a producing mine in the Yukon and a project that is way at the other end of the lifecycle and likely to stay there because of its owner's travails.

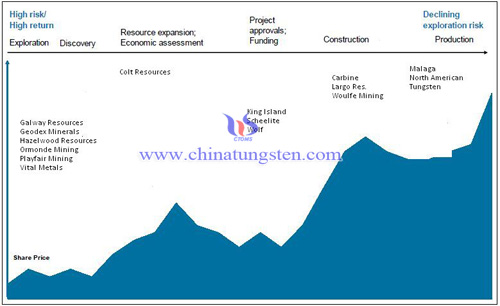

Looking back at the Lifecycle Chart (below) we published in 2011, the companies at the very right were Malaga and North American Tungsten, now both in administration or bankruptcy, and Malaga's property is in the hands of new owners.

Geodex sold its project to Northcliff. Largo mothballed its Brazilian mine almost as soon as it got into operation. Woulfe was bought by Almonty and the “other” Wolf has advanced mightily. King Island Scheelite had a management and project reconfiguration (for the better) but that has put it no further ahead of where it was. Colt has oscillated around trying to decide if it will be a Tungsten project or a gold venture. Almonty did not even figure on our radar screen!

| Tungsten Supplier: Chinatungsten Online www.chinatungsten.com | Tel.: 86 592 5129696; Fax: 86 592 5129797;Email:sales@chinatungsten.com |

| Tungsten News & Prices, 3G Version: http://3g.chinatungsten.com | Molybdenum News & Molybdenum Price: http://news.molybdenum.com.cn |

sales@chinatungsten.com

sales@chinatungsten.com